Education Loan EMI Calculator

Loan Amount

Min ₹5K

Max ₹60L

Rate of Interest

Min 6%

Max 36%

Loan Tenure

Min 3 Months

Max 72 Months

Your monthly EMI will be

₹0

Interest Amount

₹0

Principal Amount

₹30,00,000

Total Repayment Amount

₹0

Loan Amount

Min ₹5K

Max ₹60L

Rate of Interest

Min 6%

Max 36%

Loan Tenure

Min 3 Months

Max 72 Months

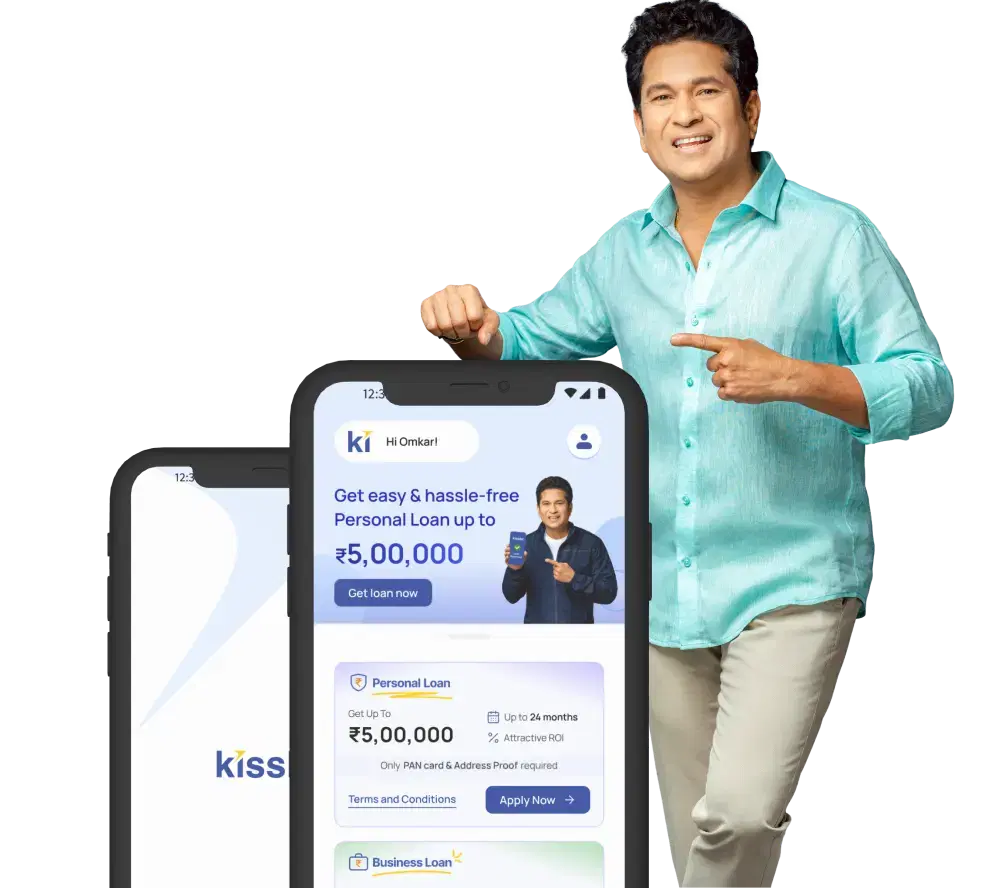

What is an Education Loan EMI calculator?

An Education Loan EMI Calculator helps students and parents estimate monthly repayments based on loan amount, tenure, and education loan interest rates. By using this tool, one can plan finances efficiently before applying for a student loan. For those exploring the best loan application for students, this tool ensures clarity in financial commitments as it offers a clear breakdown of expected payments.

Benefits of Education Loan EMI Calculator?

Comparison of Loan Options

You can analyze EMIs across different student loan apps to select the best option.

Time-Saving Tool

It eliminates manual calculations and offers instant results, streamlining the loan selection process.

Better Financial Planning

It helps students and parents assess repayment commitments before finalizing a loan.

Customizable Inputs

You can adjust loan tenure and amount to suit financial needs.

How To Calculate EMI for a Education Loan

You can quickly estimate your education loan EMI with the following details.

- Enter the Loan Amount – The amount you want to borrow.

- The Repayment Tenure – The number of months to make the repayment.

- Apply the Interest Rate – The interest rate to be applied to the loan.

- View EMI Breakdown – Structured monthly installment details.

Formula for Education Loan EMI:

Education loan EMI is calculated with the help of the following formula.

EMI = [P × R × (1+R)^N] / [(1+R)^N - 1]

Where

- P = Loan Amount,

- R = Monthly Interest Rate,

- N = Number of Months.

For example:

If you take a ₹10 lakh education loan at 12% annual interest for 5 years, the EMI would be approximately ₹22,244.

Factors that affect Education Loan EMIs

Loan Amount

The loan amount is the total amount borrowed to finance educational expenses, such as accommodation, tuition, and other academic costs. A higher loan amount leads to increased EMIs, as both the principal and interest payments rise accordingly

Opting for an amount that aligns with actual requirements ensures manageable EMIs while minimizing interest outflow. Careful evaluation helps maintain financial stability throughout the repayment period.

Credit Score

A credit score reflects an applicant’s financial credibility, while a co- applicant, often a parent or guardian, strengthens loan approval prospects. A high credit score and a financially stable co-applicant can lead to lower interest rates, reducing overall EMIs. However, a lower score may result in higher rates or stricter terms. Lenders assess both factors to determine risk, making it crucial to maintain a strong credit history and choose a co- applicant with a stable financial profile for favorable loan terms

Loan Tenure and Interest Rate

Education loan tenure determines the repayment period, and the interest rate influences the total borrowing cost. A longer tenure results in smaller EMIs but increases overall interest payments, whereas a shorter tenure raises EMIs while reducing interest expenses. The education loan interest rate, shaped by creditworthiness and lender terms, directly affects monthly repayment obligations. Selecting an optimal combination of tenure and interest rate ensures EMIs remain manageable

Moratorium Period

A moratorium period is a predefined duration during which borrowers are not required to make EMI payments, typically covering the course duration and a few months post-graduation. While this offers financial relief initially, interest accrues during this phase, increasing the total repayment amount

Opting for interest payments during the moratorium can help control future EMIs. Using an education loan calculator with a moratorium period allows borrowers to assess different repayment scenarios, ensuring a balance between immediate financial flexibility and long-term affordability

Explore other calculators

Hear from our customers

I was trying to plan my repayment after college, and the EMI calculator gave me a decent idea of what the monthly EMI would look like.

Nikhil R.

Mumbai

I didn’t expect much, but the education loan calculator actually helped me see how much interest I’d end up paying over time.

Aarushi M.

Kolkata

We were looking at loan options for my son’s course, and using the calculator made the numbers easier to understand and plan things.

Rajesh V.

Mumbai

It was helpful to try out different tenures and see how the EMI amounts changed. Made the whole process feel less intimidating.

Ishita K.

Kolkata

I was trying to plan my repayment after college, and the EMI calculator gave me a decent idea of what the monthly EMI would look like.

Nikhil R.

Mumbai

I didn’t expect much, but the education loan calculator actually helped me see how much interest I’d end up paying over time.

Aarushi M.

Kolkata

We were looking at loan options for my son’s course, and using the calculator made the numbers easier to understand and plan things.

Rajesh V.

Mumbai

It was helpful to try out different tenures and see how the EMI amounts changed. Made the whole process feel less intimidating.

Ishita K.

Kolkata

Frequently Asked Questions?

To calculate an education loan EMI, you can use the standard formula or simply try an education loan EMI calculator for quick results. It considers the education loan interest rate, education loan tenure, and amount borrowed. Tools like the one on the [Kissht](/) website make it easy to estimate repayments before you apply.

An education loan EMI Calculator works by taking key inputs—loan amount, education loan interest rate, and education loan tenure—to compute your monthly EMI using a standard formula. It’s a quick way to understand your education loan EMI without manual math.

Anyone who meets the basic student loan criteria—like age, academic background, and admission to a recognized institution—can apply. Most lenders assess your education loan eligibility based on these factors along with a co-applicant’s financial profile.

To calculate the education loan EMI for a ₹7 lakh loan over 5 years, you can use the formula: EMI = [P × R × (1+R)^N] / [(1+R)^N – 1], where P is the amount of loan, R is the interest rate, and N is the number of EMIs. Using a standard education loan interest rate of 10% per annum (or 0.0083 monthly) and a tenure of 60 months: EMI ≈ ₹14,873 You can use the education loan EMI calculator available on the Kissht website for a quick and accurate result. Disclaimer: The EMI displayed is for illustrative purposes only. Actual amounts may vary based on the applicable interest rate, loan tenure, and terms set by the lender.

Use the standard formula: EMI = [P × R × (1+R)^N] / [(1+R)^N – 1] Where: - Principal Amount = ₹15,00,000 (loan amount) - Monthly Interest Rate = Monthly interest rate (based on your education loan interest rate) - Loan Tenure = Total number of EMIs (depends on your education loan tenure) This gives you an approximate education loan EMI of ₹31,839 per month. You can also try using the education loan EMI calculator on the Kissht website. It gives quick and accurate results. Disclaimer: The EMI displayed is for illustrative purposes only. Actual amounts may vary based on the applicable interest rate, loan tenure, and terms set by the lender.

Show More FAQs

Kissht - Sapno ko Kaho YES!

4.6

60M+

Downloads

4000Cr+

Credit Given

10M+

Customers